{kind=link}

Johannah Bernstein post: "eternally proud of my father’s extraordinary aeronautical engineering. legacy. here is a photo of the Canadair Water…

Trump administration: U.S. Economy 2019 Chapter III

Written by Diana Thebaud Nicholson // February 4, 2020 // Economy, U.S. // 1 Comment

Social Security and the U.S. deficit: Separating fact from fiction (Reuters) – For decades, some of our most prominent U.S. politicians have been sounding the alarm that Social Security is an important driver of the federal budget deficit. But is that really true? (1 November 2018)

4 February

How McKinsey Destroyed the Middle Class

Technocratic management, no matter how brilliant, cannot unwind structural inequalities.

Daniel Markovits Professor at Yale Law School and the author of The Meritocracy Trap

(The Atlantic) In the middle of the last century, management saturated American corporations. Every worker, from the CEO down to production personnel, served partly as a manager, participating in planning and coordination along an unbroken continuum in which each job closely resembled its nearest neighbor. Elaborately layered middle managers—or “organization men”—coordinated production among long-term employees. In turn, companies taught workers the skills they needed to rise up the ranks. At IBM, for example, a 40-year worker might spend more than four years, or 10 percent, of his work life in fully paid, IBM-provided training.

The mid-century corporation’s workplace training and many-layered hierarchy built a pipeline through which the top jobs might be filled. The saying “from the mail room to the corner office” captured something real, and even the most menial jobs opened pathways to promotion. In 1939, for example, all save two of the grocery chain Safeway’s division managers had started their careers behind the checkout counter. At McDonalds, Ed Rensi worked his way up from flipping burgers in the 1960s to become CEO. More broadly, a 1952 report by Fortune magazine found that two-thirds of senior executives had more than 20 years’ service at their current companies.

28 January

Jean Pisani-Ferry: Explaining the Triumph of Trump’s Economic Recklessness

The Trump administration’s economic policy is a strange cocktail: one part populist trade protectionism and industrial interventionism; one part classic Republican tax cuts skewed to the rich and industry-friendly deregulation; and one part Keynesian fiscal and monetary stimulus. But it’s the Keynesian part that delivers the kick.

(Project Syndicate) …On a policymaker’s Don’t Do list, Trump ticks many more boxes than any other post-war US president.

And yet the US economy’s longest expansion on record continues. Inflation is low and stable. Unemployment is at a 50-year trough. The unemployment rate for African-Americans is the lowest ever recorded. People who had left the labor market are returning and finding jobs. And wages at the bottom of the distribution are now rising at 4% per year, notably faster than average. On a voter’s economic wish list, Trump ticks more boxes than most of his predecessors.The political question everybody is speculating about is whether this economic performance will win Trump a second term. But the equally important (and related) economic question is whether it will teach governments worldwide that reckless initiatives beat analysis-based economic policies. If it does, expertise will be ridiculed and international policy institutions will lose whatever credibility they still have. Independent central banks may well become chapels of a forgotten cult. Populists of all guises will feel emboldened.

Overall, the lesson from Trump’s apparent economic success is not that recklessness and economic nationalism should guide policies. It is that in a low-inflation, low-interest-rate environment, the room for expansionary policies is larger than usually thought; that such an environment calls for bold policymaking, rather than the usual coyness; and that policy can spur economic inclusiveness.

17 January

Joseph E. Stiglitz: The Truth About the Trump Economy

It is becoming conventional wisdom that US President Donald Trump will be tough to beat in November, because, whatever reservations about him voters may have, he has been good for the American economy. Nothing could be further from the truth.

(Project Syndicate) Today, many corporate bosses are still talking about the continued GDP growth and record stock prices. But neither GDP nor the Dow is a good measure of economic performance. Neither tells us what’s happening to ordinary citizens’ living standards or anything about sustainability. In fact, US economic performance over the past four years is Exhibit A in the indictment against relying on these indicators.To get a good reading on a country’s economic health, start by looking at the health of its citizens. If they are happy and prosperous, they will be healthy and live longer. Among developed countries, America sits at the bottom in this regard. US life expectancy, already relatively low, fell in each of the first two years of Trump’s presidency, and in 2017, midlife mortality reached its highest rate since World War II. This is not a surprise, because no president has worked harder to make sure that more Americans lack health insurance.

Trump may be a good president for the top 1% – and especially for the top 0.1% – but he has not been good for everyone else. If fully implemented, the 2017 tax cut will result in tax increases for most households in the second, third, and fourth income quintiles.

The tax cuts were supposed to spur a new wave of investment. Instead, they triggered an all-time record binge of share buybacks – some $800 billion in 2018 – by some of America’s most profitable companies, and led to record peacetime deficits (almost $1 trillion in fiscal 2019) in a country supposedly near full employment. And even with weak investment, the US had to borrow massively abroad: the most recent data show foreign borrowing at nearly $500 billion a year, with an increase of more than 10% in America’s net indebtedness position in one year alone.

8 January

The Economy Is Expanding. Why Are Economists So Glum?

At an annual gathering of the profession, researchers presented evidence and talks that amounted to warnings on the state of the record-long expansion.

(NYT) Among the thousands of economists gathered for the profession’s annual meeting, there was little celebration of Mr. Trump’s economic policies, even though unemployment is at a 50-year low, wages are rising and the economy is experiencing its longest expansion on record.

Underlying their sense of foreboding was a widespread sentiment that the current expansion is built on a potentially shaky combination of high deficits and low interest rates — and when it ends, as it is bound to do eventually, it could do so painfully.

Ms. Yellen, who assumed the presidency of the American Economic Association at the meeting, oversaw its program of panels and presentations, assembling a lineup that included several papers assessing damage from tariffs and the trade war. She said she and her colleagues rejected four proposals for every five that were submitted, choosing some that showed the benefits to advanced economies of attracting immigrants, particularly highly skilled ones, in stark contrast to Mr. Trump’s hard line on immigration to the United States.

Few of the papers presented assessed Mr. Trump’s tax law, and none of them argued, as Mr. Trump’s advisers did at similar conferences in recent years, that the tax cuts were supercharging investment.

2019

28 December

Federal Reserve says Trump’s tariffs have so far hurt more than helped

(Quartz) US president Donald Trump’s tariffs appear to have hurt US manufacturing more than they’ve helped it, according to a study by the US Federal Reserve Board released this week.

The paper, which the authors call the first comprehensive estimates (pdf) of the tariffs’ effects on manufacturing, concluded that the tariffs led to fewer jobs in the sector, as their negative effects outweighed the benefits. Manufacturers were supposed to get a boost from the protection against practices by US trading partners Trump has deemed unfair. Instead they were hampered by rising costs and retaliatory tariffs. Manufacturers working with aluminum and steel also saw their prices rise the most. According to the paper, the new tariffs accounted for 17.6% of costs for makers of aluminum sheet, and 8.4% of the costs for steel products manufactured from purchased steel. In some cases they found the rise in prices far outweighed any competitive edge the industry received.

How The Finance Prof Who Discovered The ‘Inverted Yield Curve’ Explains It To Grandma

(Forbes) Good communicators don’t start in the weeds; they start with the big picture. In this case, the big picture might sound like this:

A powerful predictor of future recessions sparked fears of an economic downturn and triggered a sell-off in the stock market.

If you don’t read or hear another word about inverted yields, the big picture sentence explains a lot. It tells you something happened that could predict an upcoming economic recession. It tells you that whatever it was, it caused investors to flee stocks. While you still don’t know the details, you have a general idea of what caused all the ruckus. You get the gist of it.

[Making] the big picture even more relevant and compelling. “Any indicator that has a record of predicting seven of the last seven recessions should matter to you,” Harvey said. 18 August 2019

25 October

US budget deficit hits nearly $1 trillion. Does it matter?

MARTIN CRUTSINGER, Associated Press

The year-over-year widening in the deficit reflected such factors as revenue lost from the 2017 Trump tax cut and a budget deal that added billions in spending for military and domestic programs.

Forecasts by the Trump administration and the Congressional Budget Office project that the deficit will top $1 trillion in the 2020 budget year, which began Oct. 1. And the CBO estimates that the deficit will stay above $1 trillion over the next decade.

Those projections stand in contrast to President Donald Trump’s campaign promises that even with revenue lost initially from his tax cuts, he could eliminate the budget deficit with cuts in spending and increased growth generated by the tax cuts.

24 October

Paul Krugman: The Day the Trump Boom Died

Why has business confidence collapsed?

The collapse in confidence began late last year, when it became clear that Trump was serious about waging trade war on China; it continued as evidence accumulated that the 2017 tax cut was a big fizzle, doing basically nothing to boost business investment and providing at most a brief sugar high to overall growth.

But the truth is that even pessimists expected the tax cut to do more good, and the trade war less harm, than they did. Why have things turned out so poorly? One answer, to which I’ve subscribed, is that in addition to its direct impacts on U.S. exports and businesses that rely on Chinese suppliers, the trade war has created damaging uncertainty. Businesses that rely on global supply chains won’t invest for fear that the trade war will get even worse; but businesses that might move in to replace imports also won’t invest for fear that Trump will eventually back down.

3 October

Paul Krugman: Here Comes the Trump Slump And he has only himself to blame.

The Trumpist trade warriors, it turns out, missed two key points. First, many U.S. manufacturers depend heavily on imported parts and other inputs; the trade war is disrupting their supply chains. Second, Trump’s trade policy isn’t just protectionist, it’s erratic, creating vast uncertainty for businesses both here and abroad. And businesses are responding to that uncertainty by putting plans for investment and job creation on hold.

So the tweeter in chief has bungled his way into a Trump slump, even if it isn’t a full-blown recession, at least so far. It’s clearly going to hurt him politically, notably because of the contrast between his big talk and not-so-great reality. Also, the pain in manufacturing seems to be falling especially hard on those swing states Trump took by tiny margins in 2016, giving him the Electoral College despite losing the popular vote.

21 August

U.S. deficit to expand by about $800 billion more than previously expected over 10 years, CBO says

20 August

Trump Says He Has Authority to Reduce Capital Gains Taxes

(NYT) Economists estimate that such a move would add $100 billion to the national debt. It would also provide the greatest benefit to the top 0.1 percent of taxpayers, according to an analysis by economists at the Penn Wharton Budget Model.

Trump’s potential recession playbook: conspiracies, lies, and scapegoats

If the economy does falter, it might not be ideal to have a president who’s going to lie about it.

(Vox) It makes sense that a regular administration might want to downplay concerns about a recession, as panicking about a recession can sometimes be a self-fulfilling prophecy.

There are also political concerns at play: For any president staring down reelection in less than 15 months, the prospect would be unnerving. But for Trump, who has staked much of his presidential success on bragging about the strength of the economy and stock market, it’s likely especially concerning.

Which is why he seems set on saying there’s nothing wrong in the first place. It’s a signal of what may happen if and when the US economy is in real trouble: Trump will probably deny it or, at the very least, place the blame on someone else, such as his hand-picked Federal Reserve chair, Jerome Powell, or the classic “fake news.”

The Trump vs. Obama economy — in 15 charts

(WaPo) President Trump constantly refers to the economy as “strong,” “terrific” and the “greatest in the history of our country,” but a closer look at the data shows a mixed picture in terms of whether the economy is any better than it was in Obama’s final years.

The economy is growing at about the same pace as it did in Obama’s last years, and unemployment, while lower under Trump, has continued a trend that began in 2011.

The best case Trump can make for improvement since he took office is higher wages. The typical American worker’s pay is finally growing more than 3 percent a year, a level not seen since before the Great Recession. Similarly, consumer and business confidence surged after Trump’s election and has remained high, and manufacturing output (and jobs) also saw a noticeable jump in 2018 after Trump’s tax cut, although manufacturing is now struggling. There’s also been a drop in the number of Americans on food stamps.

… in other areas Trump’s record does not look as rosy. Government debt and the trade deficit are climbing (while most economists don’t worry about the rising trade deficit, Trump made it a central part of his 2016 election campaign), and business investment is faltering as corporate leaders say they are wary of Trump’s trade war. The number of Americans lacking health insurance is also ticking up slightly.

Donald Trump’s Economic Anxiety

The president can scarcely afford to continue the trade war, but he can scarcely afford to end it either.

No president wants to see the economy shrink on his watch, since that’s often lethal both to legacies and to reelection prospects, but it’s an especially pointed fear for Trump, who ran for office arguing that with his business experience, he was especially well suited to running the economy. He derided the Obama administration as a bunch of amateurs who didn’t understand numbers or know how to negotiate, and he promised that, under his leadership, there would be 4 percent annual growth, and that he’d create 25 million new jobs.

Two and a half years into his term, economic growth hasn’t reached 4 percent in a single quarter, and about 6 million new jobs have been created, which is well short of what he promised and even short of growth under Barack Obama. These shortfalls aren’t necessarily Trump’s fault: As many in the press, including me, pointed out during the 2016 campaign, presidents have relatively little control over the economy. But Trump made outlandishly unrealistic promises, and voters may hold him to account for them.

The president pushed through a large tax cut in December 2017, his greatest legislative achievement, and while that likely did stimulate the economy, it proved a political flop and did not prevent the current turmoil.

One reason for the muted success of the cuts is that Trump is also working another of his levers at cross-purposes. The president does have a remarkable amount of control over trade policy, and by installing a series of tariffs and sparking a trade war with China, Trump has put a hobble on the economy.

17 August

Ross Douthat: What Happens in a Recession?

a recessionary America would find the center-left enjoying some kind of power but probably struggling to govern, a right tearing itself apart in civil war, our downscale social crisis worsening, Silicon Valley delivering substantially less than promised, and the institutions that are supposed to inform and educate struggling or in decline.

First, the easy part: Donald Trump loses re-election. What comes next? In Washington, the centrists get a surprising opportunity. Blamed and written off by left and right alike, a Trump defeat would give the capital’s dwindling band of dealmakers and moderates another chance to govern.

… outside of D.C., the immigration crisis will diminish, while the social crisis gets worse. Notwithstanding the real horrors of gang violence in their native countries, many of the people trying to cross into the United States are clearly making an economic decision when they migrate — which means, in turn, that fewer jobs here will gradually take some pressure off the southern border. But at the same time, the domestic trends that have already worsened despite a strong economy — drug overdoses, suicide rates, middle-aged mortality, the slumping birthrate — are likely to get even grimmer in a contraction. America’s social fabric hasn’t recovered from the rendings that followed 2008; a recession now would tear out the weakest stitching quickly.

Then in the commercial sphere, the venture-capital subsidy to American consumers will dry up. The Atlantic’s Derek Thompson summed up the peculiarities of this subsidy with a recent tweet: “If you work at WeWork, drive home with Uber, and then order food by DoorDash, you’re engaging with three companies that are projected to lose about $13 billion this year.” Those losses are supposed to end with an eventual leap into profitability; in a bad economy, they may end a lot more suddenly than that. Presumably a few of the many money-losing, long-game-playing Silicon Valley companies will survive a recession — but how many? …

Finally, to end close to home, my profession will be shellacked. For many newspapers and webzines struggling to make the economics of the business work, a slump now could be simply fatal. And academia, journalism’s comrade in “careers that made more sense in 1960,” could face its own reckoning, with midsize and small colleges closing and consolidating, like midsize and small newspapers.

14 – 15 August

Citing Economy, Trump Says That ‘You Have No Choice but to Vote for Me’

(NYT) President Trump doubled down on his economic argument for re-election on Thursday night amid increasing concerns about a recession, declaring that even Americans who hate him “have no choice” but to vote for him because otherwise the stock market will collapse.

With markets already wobbling over fears of a slowdown amid an escalating trade and currency war with China, Mr. Trump flew to a battleground state to defend policies that are rattling many businesses and investors and to insist that he will prolong the country’s decade-long economic expansion into a second term.

Dow posts biggest one-day drop since October as recession fears take hold

(Reuters) Dire economic data from China and Germany suggested a faltering global economy, stricken by the increasingly belligerent U.S.-China trade war, Brexit woes and geopolitical tensions.

Paul Waldman: Could managing the economy be more complicated than Donald Trump thought?

(WaPo) Let’s take a quick look around at some recent economic news:

- Yesterday, the administration announced it was delaying a planned round of tariffs on Chinese goods until after shelves are stocked for the holiday season in order to avoid price spikes in consumer goods that might make people angry. This was a tacit acknowledgment Trump has been lying in his repeated insistence that China pays the tariffs, when in fact they’re paid by American importers, who usually pass the cost increase on to consumers.

- American taxpayers are spending tens of billions of dollars to support U.S. farmers whose access to the Chinese market has been shut off by the trade war.

- Economists are increasingly worried that the trade war could set off a recession. Meanwhile, although some Chinese manufacturers have been hurt by U.S. tariffs, rather than bringing jobs to the United States, they’re looking to relocate to other low-wage countries such as Vietnam.

- The stock market tumbled today on fears that the “inverted yield curve” is signaling a coming recession: “For the first time since 2007, the yields on short-term U.S. bonds eclipsed those of long-term bonds. This phenomenon, which suggests investors’ faith in the economy is faltering, has preceded every recession in the past 50 years. It isn’t a sure thing, but it’s one of the more reliable signs that something is amiss in the economy. Recessions typically come within 18 to 24 months after the yield curve inverts, according to research from Credit Suisse.”

- A new report from the Economic Policy Institute shows that over the past 40 years, inflation-adjusted compensation for CEOs has increased by 940 percent, while compensation for the typical worker has increased only 12 percent.

Stocks Nosedive Amid Fears of a Trump-Induced Recession

Markets dropped Wednesday as the president’s trade wars weigh on global economic growth.

(New York) Ultimately, the yield curve is an indicator that reflects market participants’ assessments of certain fundamental conditions, including the economic outlook. It is not a fundamental indicator itself

The “yield curve” refers to how interest rates on Treasury bonds change with the maturity of those bonds. If you’re lending money for a longer period, you can usually expect to earn a higher interest rate. When shorter-term bonds pay higher interest than longer-term bonds, that’s an inverted yield curve. This has often been a sign of an impending recession because it shows that investors expect interest rates to fall in the near future.

A few months ago, the yield on ten-year Treasury bonds fell below the yield on a three-month Treasury bill. Today, the ten-year rate fell below the two-year yield, which is the yield-curve comparison most frequently used to forecast recessions.

Roughly, the interest rate on a long-term bond should be the average interest rate on short-term bonds that will prevail during the term of the long bond, plus a “term premium” to compensate the lender for risks associated with lending on fixed terms for a long period. The Federal Reserve controls short-term interest rates; it does not control long-term interest rates, but it does influence them by providing guidance about its future short-term interest-rate actions and sometimes by buying and selling bonds with longer maturities. In general, interest rates should be expected to fall when the economic outlook is weak, because fewer people will be interested in borrowing money.

So when the Fed has clearly telegraphed that it is about to cut short-term interest rates, it makes perfect sense that long-term bond yields would fall in anticipation of those cuts. … In particular, low and even negative global interest rates and global economic uncertainties are driving investors worldwide to buy U.S. Treasury bonds, and all that buying pushes the yields down. There has also been a reduction over time in the typical size of the term premium, meaning the economic outlook doesn’t have to move as far from neutral as it used to for the yield curve to invert.

See 8 April Research Associates Conversations: — Cam Harvey speaks to the currently inverted yield curve as an indicator of a slowing economy : One point to make about the inverted yield curve is that it doesn’t just predict recessions, it also doesn’t give a false signal—at least over the last 60 years that we’ve measured it. The recession of 1990–91, the recession of 2001, the global financial crisis—all were forecast correctly. I suppose with all the publicity the inverted yield-curve signal has gotten, investors expect this indicator to perform, and so it could actually be a self-fulfilling prophecy.

2 August

Trump’s surprise move on Thursday to impose new tariffs on Chinese imports has thrown the Federal Reserve another curveball that may force the central bank to cut interest rates more than it had hoped was necessary to protect the U.S. economy from trade-policy risks. China’s government and companies in China do not pay U.S. tariffs directly. Tariffs are a tax on imported products and are paid by U.S.-registered firms to U.S. customs when goods enter the United States. Importers often pass the costs of tariffs on to customers – manufacturers and consumers in the United States – by raising their prices. Trump has said bad trade deals with China and others have cost millions of American jobs. Here are some of the costs of Trump’s push to rewrite the terms of global trade, with China and other top trade partners

Trump’s war on legal immigration would cripple the economy

On Wednesday, he embraced a legislative overhaul to the immigration system that, if enacted, would make that goal unattainable.

Mr. Trump endorsed a bill sponsored by a pair of conservative Republican senators, Tom Cotton of Arkansas and David Perdue of Georgia, that would reduce legal immigration by about half over a decade, a shift that a broad consensus of economists believe would sap the nation’s economic vitality. It would slash the number of immigrants granted green cards for legal permanent residence to about 540,000 annually from the current level of roughly 1 million.

Halving the number of legal immigrants would deprive an array of businesses of oxygen in the form of labor — exactly the opposite strategy required for growth in an economy where productivity is stagnant and unemployment is extremely low. By drastically constricting the supply of legal immigrants, Mr. Trump’s program would also sharply intensify the demand for undocumented immigrants, for whom no wall would be an effective deterrent.

In economic terms, therefore, the legislation makes little sense, which explains why Stephen Miller, the White House senior adviser for policy, repeatedly justified it by saying that ordinary Americans would support it in a poll.

31 July

Why the Federal Reserve Cut Interest Rates for the First Time Since the Crisis

(NYT) The Federal Reserve on Wednesday cut interest rates for the first time in more than a decade, even as the economic expansion in the United States reaches record length, unemployment hovers at historic lows and consumers keep spending. Uncertainty around global growth and persistently low inflation are behind the expected move, because both pose major threats to the health of the economy at a time when the central bank has limited ammunition to fight off a downturn. It is what’s called an “insurance cut” — one that central bankers are making to keep growth chugging along.

The Fed’s main jobs are to maintain maximum employment and stable inflation. Officials have long aimed for 2 percent as the sweet spot for price gains. A little inflation is good, because it provides a buffer to keep prices from sinking during times of slow growth. Outright deflation is dangerous because it causes consumers to hoard cash, knowing that goods and services will be cheaper tomorrow.

The problem? Inflation hasn’t hit the goal sustainably since the Fed formally adopted it in 2012.

Stubbornly low inflation has also bumped up the risk that expectations for future inflation will drift lower.

American farmer: Trump ‘took away all of our markets’

(Yahoo Finance) The White House recently announced that it would be providing an additional $16 billion in aid to American farmers affected by the trade war between the U.S. and China.

Since trade tensions began in 2018, farmers have faced major financial challenges, since China was once a major U.S. agriculture buyer.

And losing customers has become a major issue. Soybean farmers have been dealing with this, as China has turned to other countries like Brazil for soybeans. Nuylen said this is also happening for wheat farmers, as China has begun importing wheat from Russian regions.

“All these countries went to different countries to get their grain,” Nuylen said. “How are we going to get the relations back with them to buy our grain again and be our customers?”

Between 2016-2017, China was the fourth-largest wheat buyer in the world, importing more than 61 million U.S. bushels. In 2019, the top U.S. export destinations for wheat include Mexico, the Philippines, Japan, and Nigeria — China is not even among the top 10.

27 July

The Trump Tax Cuts Worked (As a Scam)

In 2017, more than 27 million Americans lacked health insurance of any kind. Many of our nation’s public schools were struggling to stock their classrooms with basic supplies, or to pay their teachers a living wage, or to keep their doors open five days a week. Underfunded rehab centers were consigning desperate opioid addicts to waiting lists amidst an overdose epidemic that would kill more Americans that one year than the Vietnam War claimed over its entire duration. Half a million Americans went homeless. More than 10 million children, in the wealthiest country on Earth, lived in “food-insecure” households.

And our congressional representatives decided that the best thing they could possibly do with $1.5 trillion in borrowed money was to give large tax breaks to the wealthy and corporations (and much smaller ones to middle-class households).

There was little empirical evidence to support this argument when Republicans were making it two years ago. There is even less today. In May, the Congressional Research Service (CRS) found no sign that the Trump tax cuts made any discernible contribution to growth, wages, or business investment. Corporations did not plow their windfalls into exceptionally productive and innovative ventures. Instead, they mostly threw their handouts onto the giant pile of cash they were already sitting on, and/or returned it to their (predominantly rich) shareholders.

The economy isn’t saving Trump because he keeps getting in the way

(WaPo) Any president running for reelection with an unemployment rate of 3.7 percent, sustained economic growth and a record-breaking stock market would be a strong favorite to win a second term. President Trump is the exception.

Trump may yet win a second term, but his prospects continue to be dragged down by, well, the president himself. Is there any other way to explain the mismatch between the current economic conditions and the current mood of a divided electorate?

As good as the economy appears to be, the benefits have been spread unevenly. Unemployment is low, but many American families remain far from feeling secure economically. Whether it is rising health-care costs, college tuition, inadequate benefits or limited savings, the economic divide between the wealthiest earners and most of the rest of the country remains real.

The Pew Research Center recently produced findings about perceptions of the economy. One broad result is the continuing degree to which perceptions are shaped by political allegiance. Once Trump was elected, Republicans became dramatically more positive about the economy, and that has continued to rise. Democrats, who along with Republicans were growing somewhat more positive in the final years of the Obama presidency, see the economy much less positively.

… Friday’s economic report highlighted another potential problem for the president. Growth in the last quarter came in at 2.1 percent — respectable but short of the kinds of numbers Trump has promised. Whether there is a genuine slowdown on the horizon is debatable, but if the stimulus provided by the big tax cut has mostly run its course, the president could find himself with less favorable statistics as the election nears.

26 July

Trump adds $4.1 trillion to national debt. Here’s where the money went

(Yahoo Finance) Once President Trump signs the budget deal that was passed by the House on Thursday and is expected to be approved by the Senate in a few days, he will have added $4.1 trillion to the national debt, according to the Committee for a Responsible Federal Budget. The total national debt surpassed $22 trillion in February.

This will mark the third time that a major piece of deficit-financed legislation will get Trump’s stamp of approval. Legislation Trump has so far signed since 2017 has added $2.4 trillion to the national debt through 2029, according to CRFB, a nonpartisan public policy group.

Many investors are worried about the ballooning national debt, with 54% naming the political environment and 47% viewing national debt as their top concerns, according to a UBS second-quarter investor sentiment survey. Tax and spending policy are the main reasons for the national debt expansion from 2017 to 2029, according to CRFB.

NOT the Wall Street Journal, but still a credible report.

Oops: Trump’s “Historic” Economic Growth Downgraded To “Meh”

The Commerce Department blows up Trump’s spot as his trade war drags down GDP and his tax cuts fail to deliver.

(Vanity Fair) In February, the White House issued a press release proudly declaring that “Economic Growth Has Reached 3% for the First Time in More Than a Decade Thanks to President Donald J. Trump’s Policies.” The brag-sheet claimed that “President Trump’s policies of tax cuts, deregulation, and trade reform have generated a booming economy,” and shamed the haters (“especially from the previous administration”) who “repeatedly denied that the president’s policies would lead to this kind of economic growth.” A quote from the president proclaimed, “we’ve accomplished an economic turnaround of historic proportions.” Only, as it turns out, that’s not what happened at all!

According to revised data from Trump’s own Commerce Department, released on Friday, the haters were right and U.S. economic growth did not hit the administration’s 2018 goal of 3% growth or higher. While the White House had initially crowed about reaching its target when it thought GDP for the fourth quarter had risen to 3.1%, on Friday that was revised to 2.5%, meaning the economy grew only 2.9% last year. Awkward!

The Commerce Department also said that the economy grew more slowly than previously thought for the second quarter of 2018, at an annual rate of 3.5% rather than 4.2%, largely due to lower exports and weaker investment in structures than expected.

As the Wall Street Journal notes, the fourth quarter was a rocky time for consumers thanks to, among other things, worry about trade tensions (caused by Trump) and the start of a government shutdown (caused by Trump), in addition to signs of global economic slowdown. The revised numbers also hurt the administration’s claims that that a $1.5 trillion tax cut would pay for itself in economic growth.

25 July

Paul Krugman: Trump’s Secret Foreign Aid Program

He’s giving away billions to overseas investors.

… Trump’s tariffs aren’t a tax on foreigners, whatever he may think. On the other hand, his other policies have given selective foreigners a huge tax break.

Remember, Trump’s only major legislative achievement so far is the 2017 Tax Cut and Jobs Act. The core of that bill was a sharp reduction in corporate tax rates, which has led to a drastic fall in tax revenues, on the order of $140 billion over the past year.

… who is benefiting from the tax cut? Basically, shareholders, who have received increased dividends and seen a lot of capital gains as corporations use their windfall not to invest, but to buy back their own stocks.

And a big share of these gains to shareholders has gone to foreigners.

We live, after all, in an era of globalized finance, in which wealthy investors normally own assets in many countries. … Over all, foreigners own about 35 percent of the equity in corporations subject to U.S. taxes. And as a result, foreign investors have received around 35 percent of the benefits of the tax cut. As I said, that’s more than $40 billion a year.

4 July

Trump’s two new Fed nominees – One, Chris Waller, should be a “no brainer” for confirmation; he has taught at Notre Dame & the University of Kentucky & since 2009 has been at the St. Louis Fed, most recently as EVP & Director of Research (at possibly the most research-oriented Federal Reserve Bank) & is a known ‘dove’. The other, Judy Shelton, may be a longer shot and not for a lack of educational qualifications (she has a Ph.D. in Business Administration), nor because she is such a blatant Trump acolyte. But her thinking seems for sale : while during the Obama years she criticized low interest rates, in the Trump era she’s in favour of them and, while once she advocated free trade, she now supports the trade war on China. Moreover, she’s a gold “nut” who earlier this year went on record as saying she was hoping for “a new Bretton Woods -style conference where countries would agree to a return to the gold standard” (& “if it takes place at Mar-a-Lago, that would be great”). All of this combined should be deemed, & hopefully will be seen, by the Senate as limiting her scope for being a productive Federal Reserve Board Governor. —Nick Rost van Tonningen Gleanings 815

26 June

Trump Redoubles Attacks on Fed Chair, Saying ‘I Made Him’

(NYT) A day after Federal Reserve Chair Jerome H. Powell asserted his independence from the White House, President Trump responded by suggesting that nobody had heard of Mr. Powell until Mr. Trump tapped him to run the Fed and implying that the head of Europe’s central bank was making better decisions. Mr. Trump also voiced jealousy over Europe’s monetary policy. Last week, he criticized Mario Draghi, the head of the European Central Bank, for saying the bank was prepared to prop up Europe’s economy unless it improves. Mr. Trump said Mr. Draghi was trying to push down the value of the euro to give Europe an unfair advantage. … On Wednesday, Mr. Trump directed all his fire at Mr. Powell, whom he accuses of not doing enough to help boost the American economy. Mr. Trump, who has pinned his re-election hopes on economic growth, has blamed Mr. Powell for working at cross-purposes with his policies, including his $1.5 trillion tax cut and increased government spending.

19 June

Trump honors Reagan economist Arthur Laffer with Medal of Freedom

(CNN)President Donald Trump on Wednesday honored economist Arthur Laffer, a former adviser to Ronald Reagan who is known as the father of supply side economics, with the Presidential Medal of Freedom.

“Few people in history have revolutionized economic thought and policy like Dr. Art Laffer. He developed a brilliant theory, shaped unprecedented economic reforms and helped turn a severe recession into a remarkable boom,” Trump said during an Oval Office ceremony to award Laffer with the nation’s highest civilian honor.

The President also claimed that Laffer’s work “spurred economic reforms around the world and helped lift untold millions out of poverty,” though other factors contributed to tax cutting and deregulation around the globe at that time.

Accepting the medal, Laffer — who was also the first chief economist of the Office of Management and was a consultant to the Treasury and Defense departments — thanked his family and many of his “teammates,” which include several Trump administration economic advisers and Cabinet members, as well as former Vice President Dick Cheney and economist Milton Friedman.

4 June

Trump Is Slowing US Economic Growth

By Robert J. Barro

The current state of US macroeconomic policymaking across four key areas does not bode well. Although the 2017 tax legislation has done its job in promoting faster growth, rising trade tensions, persistent regulatory burdens, and a lack of investment in infrastructure all threaten to limit the US economy’s potential.

(Project Syndicate) As for infrastructure, the potential benefits to US productivity from increased investment are real. Yet nothing has happened. The situation is best encapsulated by an April meeting between Trump and congressional leaders. According to media reports, Trump began by proposing to spend $1 trillion on infrastructure, whereupon the Democrats countered by suggesting $2 trillion. Trump apparently agreed to that with little hesitation. All in all, the exchange confirms, once again, that both parties have come to regard government spending as a free lunch, at least when it is financed by debt or the creation of new money. Perhaps it is actually for the best that “Infrastructure Week” never goes anywhere.

7 May

Trump has reached an inflection point in his presidency

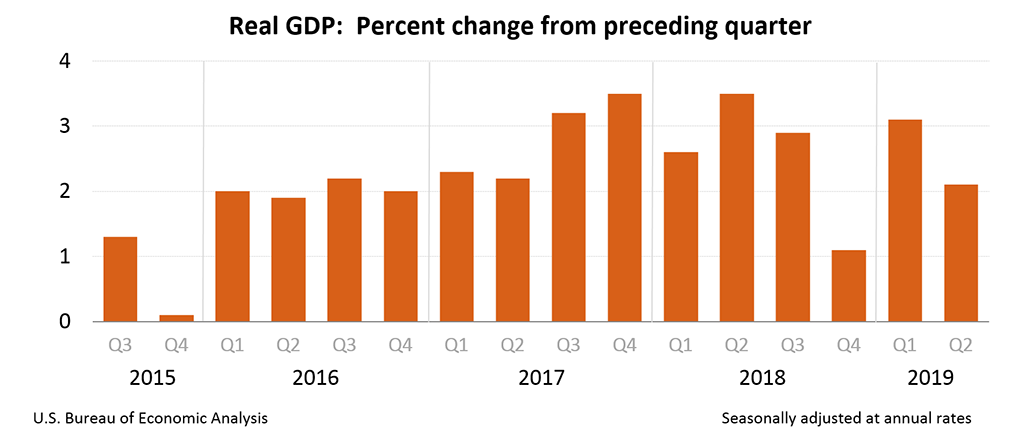

By Marc A. Thiessen

(WaPo) On Friday, we learned that the economy added 263,000 jobs in April — exceeding the 190,000 that economists predicted. This came on top of the news, a week earlier, that the U.S. economy grew at an annual rate of 3.2 percent in the first quarter, far exceeding predictions of 2.5 percent growth. Unemployment is at the lowest level in five decades. In fact, America’s biggest economic problem is that, according to The Post, “the United States has more job openings than unemployed people” to fill those jobs.

Not only are people finding work, but their paychecks are growing. In April, wages rose 3.2 percent, the ninth straight month of above 3 percent wage growth. And the Wall Street Journal reports that wages for Americans without a high school diploma rose more than 6 percent last year, outpacing all other groups.

Here is the bad news for Trump: While approval for his handling of the economy reached a new high of 56 percent, his overall job approval is still a dismal 45 percent, according to a CNN poll. Despite the booming economy, a 54 percent majority still disapprove of Trump’s presidency.

… Trump needs to focus on a positive agenda to improve the lives of Americans, draw attention to his accomplishments rather than his controversies, and reach out and try to work with Democrats. He needs to keep the economy moving, which is why the $2 trillion infrastructure package he announced with “Chuck and Nancy” is so appealing to the president. For Trump, it is a win-win — blue-collar jobs and Keynesian economic stimulus.

30 April

It’s Infrastructure Week!

Mr. Trump, here’s a fight worth having.

(NYT editorial board) On Tuesday, a dozen Democratic lawmakers, including the House speaker, Nancy Pelosi, and the Senate minority leader, Chuck Schumer, headed to the White House for a frank talk with President Trump about the “I” word: infrastructure. … Ms. Pelosi proclaimed her team “very excited about the conversation” and cheered Mr. Trump for agreeing that a “big and bold” plan was needed. Mr. Schumer called the meeting “constructive” and noted approvingly that the president had been “eager” to push funding up to $2 trillion. “This was a very, very good start,” Mr. Schumer told reporters.

As part of branding himself an economic populist, Mr. Trump campaigned in 2016 with a vow to spend $1 trillion to make America’s roads, airports and transit systems the envy of the world. He blew into office with grand visions of launching development projects across the nation. … But, thus far, Mr. Trump has proved very bad at building. Highways, bridges, pipelines, water systems, even beautiful steel border walls — all have turned out to be more complicated than he anticipated. Infrastructure policy was repeatedly pushed to the side during his first year in office, turning the phrase “Infrastructure Week” into a sad joke. And his administration’s 2018 plan fell flat. The $1.5 trillion package provided a paltry $200 billion in federal funding, relying heavily on public-private partnerships and state spending. No one in Congress was interested in championing it. Even the president publicly questioned its feasibility.

25 April

Political gridlock blocks infrastructure progress and costs our economy

(Brookings) Infrastructure talks are heating up again. In just the last week, 2020 presidential candidate Amy Klobuchar pitched a trillion-dollar infrastructure proposal while the Trump administration and Congress continue to flirt with major infrastructure packages. This kind of thinking reflects clear public support for greater investment. While these concepts and conversations suggest bipartisanship could deliver infrastructure reform, the current state of national politics delivers anything but an infrastructure boost. Put bluntly, when political discord leads to infrastructure failure, it doesn’t just deepen our distrust of government—it also takes our economy down with it.

This administration’s trade and tariff policies serve as a potent example of self-inflicted economic harm. Since the Trump administration applied tariffs on imported steel and aluminum, the cost index for steel mill products alone rose by almost 14 percent from March 2018 to January 2019. This directly impacts our state departments of transportation, their local peers, and water authorities who all rely on steel and aluminum to construct major capital projects. As Mark Niquette at Bloomberg reported, states from California to Michigan to Virginia have already seen certain project costs jump by millions of dollars. Meanwhile, steel and aluminum manufacturers in the U.S. have been hit hard by the costs, needing to lay off workers to close budget gaps.

2 April

Trump Vows to Close Border, Even if It Hurts the Economy

“Sure, it’s going to have a negative impact on the economy,” Mr. Trump said, adding, “but security is most important.”

“Security is more important to me than trade,” he said.

Republican lawmakers, economists and business groups largely disagree with that assessment and warned this week that closing the border could cripple the flow of goods and workers and devastate American automakers and farmers, as well as other industries that depend on Mexico for sales and goods.

“Closing down the border would have a potentially catastrophic economic impact on our country,” Senator Mitch McConnell, Republican of Kentucky and the majority leader, said in an interview. “I would hope that we would not be doing that sort of thing.”

Mark Zandi, the chief economist at Moody’s Analytics, said that “a full shutdown of the U.S.-Mexican border of more than several weeks would be the fodder for recessions in both Mexico and the U.S.”

Avocado shortages, virgin margaritas: Border shutdown would hit American palates

22 March

Jonathan Chait: Trump Nominates Famous Idiot Stephen Moore to Federal Reserve Board

(New York) Stephen Moore’s career as an economic analyst has been a decades-long continuous procession of error and hackery. It is not despite but precisely because of these errors that Moore now finds himself in the astonishing position of having been offered a position on the Federal Reserve board by President Trump.

Moore’s primary area of pseudo-expertise — he is not an economist — is fiscal policy. He is a dedicated advocate of supply-side economics, relentlessly promoting his fanatical hatred of redistribution and belief that lower taxes for the rich can and will unleash wondrous prosperity. Like nearly all supply-siders, he has clung to this dogma in the face of repeated, spectacular failures.

He is capable of writing entire columns that contain no true facts at all. He made so many factual errors he achieved the rare feat of being banned from the pages of a Midwestern newspaper. He has sold his policy elixir to state governments which have promptly experienced massive fiscal crises as a direct result of listening to him. … And yet, for all their extravagant ignorance, Moore’s beliefs on fiscal policy are actually more sophisticated and well-developed than his views on monetary policy. It is the latter that he would be in a position to influence as a Federal Reserve governor.

11 March

Trump Proposes a Record $4.75 Trillion Budget

The new Trump budget is a horror show

(WaPost) the Trump administration just released contains enormous cuts to Medicare and Medicaid, not to mention domestic programs. In a word, it is positively savage. Some of the highlights:

The Trump budget would cut about $845 billion from Medicare over 10 years

It cuts $241 billion from Medicaid

It would push Medicaid toward block grants which cap the amount each state would receive, which when the money runs out would result in pared-back benefits, recipients being tossed off the program or both

It would eliminate the Affordable Care Act’s expansion of Medicaid, which would mean millions would lose their health coverage

It would cut $25 billion from Social Security

It would impose work requirements on recipients of food stamps, Medicaid and housing assistance, forcing them to navigate a bureaucratic maze or lose their benefits

It would cut $220 billion from food stamps

It would cut $1.1 trillion from domestic discretionary programs, which do not include Medicare, Medicaid or Social Security

It would cut the Department of Housing and Urban Development by 16 percent and the Education Department by 12 percent

It would cut the Environmental Protection Agency by 31 percent

Trump’s budget is heartless and whackadoodle

(WaPost) …based on this latest statement, Trump’s priorities continue to be redistributing wealth ever upward, from poor to rich, and selling the public more fantasies and lies.

Federal deficits have widened immensely under Trump’s leadership. This is striking not only because he promised fiscal responsibility — at one time even pledging to eliminate the national debt within eight years — but also because it’s a historical anomaly. Deficits usually narrow when the economy is good and we’re not engaged in a major war.

Trump’s own policies are to blame for this aberration. Specifically, the 2017 tax law, which gave two-thirds of its benefits to the top income quintile last year, added $1.9 trillion to deficits over the coming decade. A grand-bargain spending bill last year that increased funding for both defense and nondefense programs — here the Democrats deserve a share of the blame — also spilled plenty of red ink.

Trump’s plan for addressing these issues? Extend the plutocratic tax cuts (currently slated to partially expire in 2025), which would add $1 trillion to deficits; double down on defense spending increases (and money for his border wall); and then balance the budget on the backs of the nation’s most vulnerable.

and, of course:

Trump calls for cutting National Science Foundation funding by $1 billion

8 March

The tax cuts will make fighting future recessions complicated

(Brookings) … The tax cuts will also hamper the ability to fight recessions in other ways. With higher deficits, political leaders will be more reluctant to engage in discretionary stimulus programs to boost the economy. By making some typical instruments, such as expensing, part of the tax code, the tax cuts reduce the number of tools that policymakers can use to fight downturns. A recent paper by two economists with the Joint Committee on Taxation shows that the subsidies for foreign derived intangible income operates in a procyclical fashion by rising during booms and falling during recessions, precisely the opposite of how automatic fiscal stabilization should work.

In one way, it is fitting that the 2017 tax law has poor cyclical properties. Indeed, the deficit financed tax cuts were enacted and implemented at a time when the economy was already doing very well, exactly the opposite of how strong stabilization should work.

12 February

Debt surpasses $22 trillion for first time

“This milestone is another sad reminder of the inexcusable tab our nation’s leaders continue to run up and will leave for the next generation,” said Judd Gregg and Edward Rendell, co-chairman of the debt watchdog group Campaign to Fix the Debt.

Deficits have soared under President Trump, spurned on by the GOP tax law, bipartisan spending increases, and the forward momentum of mandatory spending programs such as Medicare and Social Security. Tuesday’s estimate put the total outstanding public debt at $22.013 trillion,

11 February

Trump Trade War Helps Push Farmers Into Record Number Of Bankruptcies

Dairy farmers were counting on China milk buyers before the trade war. “The problem is both nations have stubborn leaders,” an industry analyst said.

(HuffPost) Twice as many farmers in Illinois, Indiana and Wisconsin declared bankruptcy last year compared to 2008, according to statistics from the 7th Circuit Court of Appeals, the Journal reported. Bankruptcies in states from North Dakota to Arkansas leaped 96 percent, according to figures from the 8th Circuit Court of Appeals.

Farmers are being battered by sinking commodity prices — and stiff tariffs from China and Mexico in retaliation for Trump’s tariffs on imports.

The new 11-nation Comprehensive and Progressive Agreement for the Trans-Pacific Partnership (CPTPP) treaty last year slashed tariffs — but not for U.S. farmers since the Trump administration pulled out of negotiations. That drove customers to farmers and ranchers in competitive countries, like Australia, serving another dunning blow to American operations.

6 February

Middle Class Dads Freak Out About Trump Tax Hike

(Yahoo)…some people have already managed to file their taxes. And among those early birds, many in the middle class have been shocked to find that instead of the nice little chunk of change they were expecting with their return, they actually owe money to Uncle Sam…. It stems from President Trump’s tax reform, which was passed in 2017 and was touted by Trump and the GOP as a win for the middle class. However, with the new tax system now in place, Americans are discovering that most of the tax relief from the bill is actually being experienced by corporations.

Meanwhile, many people are seeing an increase in taxes due to the bill eliminating many of the deductions that were used by middle-class families in order to lower the amount of taxes they were required to pay. Most notably, the tax reform placed a cap on deductions for taxes on both state and local levels.

28 January

Government shutdown cost US economy $11bn

Annual growth forecast revised down 0.2%

Congressional Budget Office says full effect may be larger

(The Guardian) According to the CBO, the shutdown hurt economic growth because it affected roughly 800,000 workers and delayed federal spending on goods and services.

Much of the money will be recouped now the government is open again but the CBO calculates $3bn will never be recovered and the full impact of the closure – which left hundreds of thousands of federal workers and contractors without pay – may be larger.

The CBO warned “all of the estimated effects and their timing are subject to considerable uncertainty”.

The five-week shutdown delayed approximately $18bn in federal discretionary spending for compensation and purchases of goods and services and suspended some federal services.

As a result of the delay in wages and spending, the CBO expects the level of gross domestic product (GDP) – the broadest measure of economic growth – to fall by 0.2% in the first quarter of the year.

$1.5 trillion U.S. tax cut has no major impact on business capex plans: survey

(Reuters) The Trump administration’s $1.5 trillion cut tax package appeared to have no major impact on businesses’ capital investment or hiring plans, according to a survey released a year after the biggest overhaul of the U.S. tax code in more than 30 years. “A large majority of respondents, 84 percent, indicate that one year after its passage, the corporate tax reform has not caused their firms to change hiring or investment plans,” said The National Association of Business Economics’ President Kevin Swift.

Shutdown Damage Will Persist Long After U.S. Government Reopens

From science and parks to natural disasters, damage to linger

‘Loss of a workforce that is not interested in public service’

(Bloomberg) The government may be reopening, but the consequences of the longest federal shutdown in U.S. history are likely to linger for national parks, forests, the federal workforce and cutting-edge scientific research. Some may even be permanent.

Many fire crews missed their window for controlled burns to prevent wildfires. Irreplaceable relics may have been damaged in unguarded national parks. Science experiments were abandoned. And a generation of talent may now think twice about signing up for government, while workers returning to a month of unopened emails and missed meetings will have to decide which of their priorities to sacrifice this year.

The shutdown could also make it harder for the government to find contractors with the skills it needs, said David Berteau, president of the Professional Services Council, a group that represents federal contractors. “Many of them may begin to look for — and will take — jobs in the private sector,” he said.

23 January

CEOs sour on Trump policies, warn they hurt business, investment

(Reuters) Foreign investment in the United States, which includes cross-border mergers and acquisitions and intra-company loans, fell about 18 percent in 2018 from the prior year, according to the United Nations Conference on Trade and Development (UNCTAD).

That is close to the 19 percent year-on-year drop in foreign investment globally. But it is notable given the deregulation and tax cuts that might have otherwise fed into inward investment. In January of last year, at Davos, many executives said they planned to spend money in the U.S. in 2018.

16 January

Shutdown bites economy, U.S. Coast Guard, as talks to end impasse stall

(Reuters) – The U.S. economy is taking a larger-than-expected hit from the partial government shutdown, White House estimates showed on Tuesday, as contractors and even the Coast Guard go without pay and talks to end the impasse seemed stalled.

With the shutdown dragging on, federal courts will run out of operating funds on Jan. 25 and face “serious disruptions” if the shutdown continues, according to a court statement.

While the shutdown hit about one-quarter of federal operations, a Reuters/Ipsos poll released on Tuesday found that nearly four in 10 U.S. adults said they were either affected by the impasse or know someone who is. Fifty-one percent of those polled blamed Trump for the shutdown.

The Trump administration had initially estimated the shutdown would cost the economy 0.1 percentage point in growth every two weeks that employees were without pay.

But on Tuesday, there was an updated figure: 0.13 percentage point every week because of the impact of work left undone by 380,000 furloughed employees as well as work left aside by federal contractors, a White House official said.

Shutdown raises the risk of recession

(Politico) The partial federal government shutdown could be the kind of shock to consumer and business confidence that helps nudge the economy toward the next recession, according to a leading economist who served under former President Barack Obama.

Historically, government shutdowns have had limited impact on the overall economy. But the duration and severity of the current impasse, now more than three weeks old, has led some economists to suggest it could cause deeper damage.

Shutdown’s Economic Damage Starts to Pile Up, Threatening an End to Growth

(NYT) The partial government shutdown is inflicting far greater damage on the United States economy than previously estimated, the White House acknowledged on Tuesday, as President Trump’s economists doubled projections of how much economic growth is being lost each week the standoff with Democrats continues.

The revised estimates from the Council of Economic Advisers show that the shutdown, now in its fourth week, is beginning to have real economic consequences. The analysis, and other projections from outside the White House, suggests that the shutdown has already weighed significantly on growth and could ultimately push the United States economy into a contraction.

While Vice President Mike Pence previously played down the shutdown’s effects amid a “roaring” economy, White House officials are now cautioning Mr. Trump about the toll it could take on a sustained economic expansion. Mr. Trump, who has hitched his political success to the economy, also faces other economic headwinds, including slowing global growth, a trade war with China and the waning effects of a $1.5 trillion tax cut.

4 January

US national debt rises $2 trillion under Trump

(CNN) The US national debt stood at $21.974 trillion at the end of 2018, more than $2 trillion higher than when President Donald Trump took office, according to numbers released Thursday by the Treasury Department.

The national debt has been rising at an accelerated rate in the aftermath of the 2008 financial crisis, when Congress and the Obama administration approved stimulus funding in order to keep the economy afloat.

The debt began to level off at the beginning of Trump’s term, but bounced up again last year as the tax cuts passed at the end of 2017 took effect and the dramatically lower corporate tax rate lowered Treasury revenues.

As a candidate, Trump promised to “get rid of” the national debt, telling the Washington Post in 2016 that he could make the US debt-free “over a period of eight years.”

According to the Congressional Budget Office, total public debt stood at 78% of America’s gross domestic product in fiscal year 2018, the highest percentage since 1950. The deficit — or the difference between what the government spends and what it takes in over any one year — jumped to 3.8% of GDP in 2018, up from 3.5% in 2017.

That’s particularly unusual in such a strong economy without major new expenditures. If no changes are made, the CBO projects that public debt will rise to 96% of GDP by 2028. A big chunk of that — $1.9 trillion between 2018 and 2028 — will be due to the Tax Cuts and Jobs Act, the CBO reported last April. [See Jan 16 Comment from Christopher Goodfellow below]

One Comment on "Trump administration: U.S. Economy 2019 Chapter III"

Christopher Goodfellow on Facebook:

He doesn’t care but you should. You will pay for it through inflation. A great effort should be made to balance the budget and bring it into surplus. Remember 100$ million spent on infrastructure brings many economic spinoffs. 100$ spent on bombs yield nothing. If we do not tax to cover expenditures and just print money to pay the interest, it will not end pleasantly.